Contra Costa Plan B

ContraCostaplanB.com presents a detailed, publicly trackable alternative to Measure B — one that addresses the county’s budget pressures through phased spending management, without raising the county sales tax. One key element: the county already holds more than enough in general fund reserves to absorb near-term federal and state funding losses.

How the reserve figure is calculated

The county’s unreserved general fund balance as of June 30, 2025 totals $1,189,653,000, composed of three components:

- Nonspendable fund balance: $1,078,000

- Committed fund balance: $604,025,000

- Assigned fund balance: $584,550,000

The county’s general fund expenditures for fiscal year 2024–25 were $2,319,352,000. That puts the reserve ratio at 51.3% — more than three times the 16.7% (two months of expenditures) recommended by the Government Finance Officers Association as a minimum prudent reserve.

The county could draw down hundreds of millions without jeopardizing its fiscal health

Even if the county drew down $400 million of its reserves over the five-year life of Measure B — $80 million per year — it would still hold reserves well above the GFOA minimum. The county’s own projected federal and state health funding losses average far less than $80 million per year in the near term. Per the county’s corrected March 3 figures, the cumulative health services shortfall through fiscal year 2028–29 is approximately $239 million — roughly $60 million per year.

Reserves exist precisely for situations like this

The Government Finance Officers Association and most public finance professionals advise maintaining reserves of two months of expenditures (16.7%) as a floor — the minimum needed to handle normal revenue volatility and short-term shocks. Contra Costa’s 51.3% reserve ratio reflects a cushion that is three times that floor.

Temporary, phased revenue losses from federal and state policy changes — especially when those changes are still being implemented and are subject to legal challenge, Congressional revision, and state mitigation — are exactly the kind of situation for which general fund reserves exist. Locking in five years of higher sales taxes before the full scope of cuts is even known is fiscally premature.

The biggest driver of the county’s budget gap is not health funding

According to the county’s own January 2026 budget development presentation, the largest single component of the projected FY 2026–27 budget pressure is not federal health cuts — it is rising employee pay and benefits, estimated at $208 million in FY 2026–27 alone and growing at roughly 5% per year. Federal and state health impacts in the first year total approximately $42 million combined.

Asking every Contra Costa resident and visitor to pay a higher sales tax — in part to subsidize growing county employee compensation — is a policy choice, not a fiscal necessity.

Sources

- Contra Costa County Comprehensive Annual Financial Report (CAFR), fiscal year ending June 30, 2025 — general fund balance components

- Government Finance Officers Association, Best Practice: Fund Balance Guidelines for the General Fund

- Contra Costa County FY 2026–27 Budget Development Key Considerations (Jan. 30, 2026)

- Resolution 2026-40, Recital H (revised March 3, 2026) — $239M cumulative Health Services shortfall through FY 2028–29

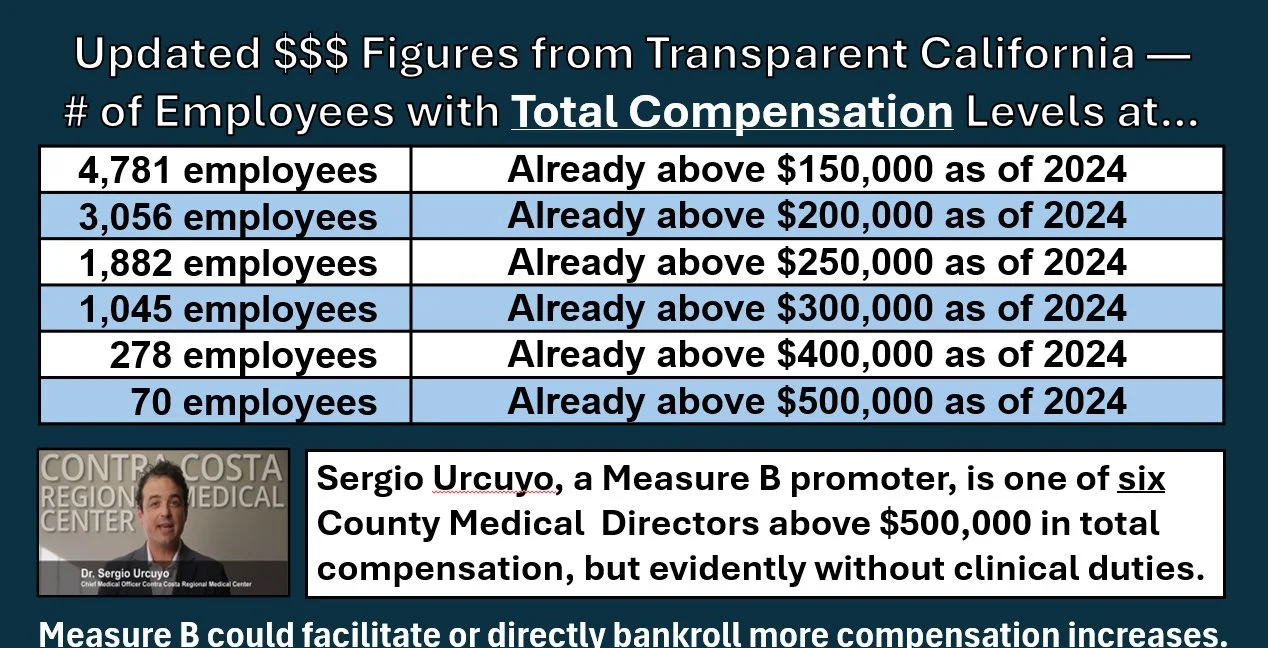

- Transparent California — Contra Costa County employee compensation data (2024)

- ContraCostaplanB.com — Contra Costa Plan B, including budget pressure methodology and charts